Mazzone advises Rayven Inc. on its sale to Duraco Specialty Tapes

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as exclusive financial advisor to Rayven Inc. (“Rayven”), a developer and manufacturer of engineered packaging coatings, tapes, and release liners, on its sale to Duraco Specialty Tapes (“Duraco”), a leading manufacturer of pressure-sensitive tapes and specialty materials.

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as exclusive financial advisor to Rayven Inc. (“Rayven”), a developer and manufacturer of engineered packaging coatings, tapes, and release liners, on its sale to Duraco Specialty Tapes (“Duraco”), a leading provider of pressure-sensitive tapes, labels and coated films.

Rayven, headquartered in St. Paul, Minnesota, offers custom developed, niche release liners, coated functional films, and pressure-sensitive adhesive tapes to a diverse portfolio of high-value end markets including flexible packaging, medical device, specialty building, and graphics.

“We are excited to partner with the strong operational teams at Duraco and OpenGate, who share our culture and entrepreneurial values, as well as our drive to create and deliver innovative products for our customers,” said Rayven President Joe Heinemann, who will remain in that role. "Our thanks to the Mazzone team for guiding our family through this process. Their insight and advice were instrumental in assuring a smooth process and a successful sale.”

OpenGate Capital acquired Duraco in June 2019 as a corporate carveout from Essentra PLC and has since completed four add-on acquisitions with Infinity Tapes in February 2020, Filmquest Group in March 2021, 3 Sigma in November 2021 and now Rayven.

The combination of these acquisitions and organic investments have significantly advanced Duraco’s core capabilities across formulation, coating, converting and distribution. With these investments, the Company is now positioned as an integrated, turnkey solutions provider in its markets with technology, product portfolio and capacity to drive growth with existing and future customers.

Ed Byczynski, Chief Executive Officer of Duraco, stated “The addition of Rayven builds on Duraco’s leadership position as a high-quality, custom manufacturer of coated flexible packaging film, niche release liners and specialty tapes in North America, and will expand Duraco’s developmental capabilities and add coating capacity to support the ongoing growth of the collective businesses.”

“Rayven is the latest testament to our focus on add-on investments as an accelerator of growth,” said Andrew Nikou, OpenGate Capital’s Founder and CEO. “The combination of Rayven’s operational capabilities, along with Duraco’s strong operating expertise and its seasoned management team will drive continued commercial growth into new markets.”

About Rayven

Rayven Inc. has over 60 years of experience manufacturing custom silicone release liners and PSA products. Founded in 1954, Rayven grew from one coating line for producing polyester label stock, to 2 manufacturing plants; one in St. Paul, Minnesota and its newest facility in Owatonna, Minnesota. Rayven supplies finished material ranging from letter sized sheets to slit rolls of all sizes.

About Duraco Specialty Tapes

Duraco is B2B manufacturer of pressure-sensitive tapes and specialty materials, which are sold into highly attractive end markets including Point-of-Purchase displays, appliances, transit packaging, construction, signage and HVAC. Duraco’s application- specific tapes are strong alternatives to mechanical fasteners and traditional glues offering longevity, strength, efficiencies in customer’s assembly operations and breadth of substrates. In 2020, Duraco expanded its capabilities with the acquisition of Infinity Tapes, a leading manufacturer of customized adhesive products serving the high growth industrial and transit packaging end markets. Duraco is headquartered in Forest Park, IL. With warehousing locations throughout the United States and Canada, Duraco has a workforce of over 200employees and has been maintaining loyal relationships for over 40 years and is continuously growing with over 6,800 customers. To learn more about Duraco, please visit www.duraco.com.

About OpenGate Capital

OpenGate Capital is a global private equity firm specializing in the acquisition and operation of businesses to create new value through operational improvements, innovation, and growth. Established in 2005, OpenGate Capital is headquartered in Los Angeles, California with a European office in Paris, France. OpenGate’s professionals possess the critical skills needed to acquire, transition, operate, build, and scale successful businesses. To date, OpenGate Capital has executed more than 30 acquisitions across North America and Europe. To learn more about OpenGate, please visit www.opengatecapital.com.

More Recent Packaging Industry Transactions

Industry Insights: Global Packaging Update Fall 2021

2021 has witnessed remarkable rebounds for the economy generally, the transaction market overall, and specifically for the Packaging Transaction Market. The economy rebounded particularly well through mid-year 2021, with the US GDP growing over 6% in each of Q1 and Q2 and defying the rise of the delta variant, inflationary pressures, supply chain disruptions, and a disconnect between labor demand and willing workers. This success was mirrored in the deal-making marketplace, particularly among financial sponsors (Private Equity), which drove volumes that will surpass 2019's former annual record [i]. Acquirers are riding the high economy, a very favorable lending environment, and sellers seeking to avoid a potential increase in tax rates in 2022.

2021 has witnessed remarkable rebounds for the economy generally, the transaction market overall, and specifically for the Packaging Transaction Market. The economy rebounded particularly well through mid-year 2021, with the US GDP growing over 6% in each of Q1 and Q2 and defying the rise of the delta variant, inflationary pressures, supply chain disruptions, and a disconnect between labor demand and willing workers. This success was mirrored in the deal-making marketplace, particularly among financial sponsors (Private Equity), which drove volumes that will surpass 2019's former annual record [i]. Acquirers are riding the high economy, a very favorable lending environment, and sellers seeking to avoid a potential increase in tax rates in 2022.

Market Review: Sustainability in Packaging

In this summary, we highlight trends, developments and M&A activity within the sustainable packaging market including key trends in the supply chain and in regulation, mergers and acquisitions activity, and investment opportunities within the sustainable ecosystem.

Mazzone and Associates understands the key trends and pitfalls in the sustainable packaging market with recent deal experience as well as long-standing industry knowledge. In this summary, we highlight trends, developments and M&A activity within the sustainable packaging market including key trends in the supply chain and in regulation, case studies in mergers and acquisitions activity, and investment opportunities within the sustainable ecosystem.

Recent Packaging Industry Transactions:

Join Our Packaging Mailing List

Enter your email address below to receive our packaging industry newsletters, market reviews, and updates

Mazzone & Associates Advises Roplast on its Sale to PreZero

Robert Bateman, retired CEO and co-founder of Roplast, reflected on the transaction: “We are quite satisfied with the result and Roplast’s new partnership with PreZero. In these uncertain times, the Mazzone team proved invaluable, providing guidance and driving the marketing process with domestic and international parties. I doubt whether anyone could have advised us better.”

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as the exclusive financial advisor to Roplast Industries, Inc. (“Roplast” or the “Company”) with respect to its sale to PreZero US (“PreZero”), a subsidiary of the parent company Schwarz Group, headquartered in Neckarsulm, Germany. The terms of the transaction were not disclosed.

PreZero and Roplast come together just as increasing U.S. legislation will be requiring more recycled content in packaging. As noted by PreZero’s press release, this transaction reflects “PreZero’s business goal to vertically integrate and deliver its closed loop solutions to support the circular economy.”

Robert Bateman, retired CEO and co-founder of Roplast, reflected on the transaction: “We are quite satisfied with the result and Roplast’s new partnership with PreZero. In these uncertain times, the Mazzone team proved invaluable, providing guidance and driving the marketing process with domestic and international parties. I doubt whether anyone could have advised us better.”

Robert Berman, co-founder of Roplast, commented “We are excited for Roplast and its future prospects with its new partner. The Mazzone team did a great job at understanding our business and market position in sustainable packaging. They were extremely thorough and did an outstanding job guiding our team and ensuring the transaction ran smoothly for all parties.”

Jonathan White, Managing Director at Mazzone & Associates, noted “We invested significant time to identify the right partner for our client. We found a great fit in Schwarz and PreZero, as they will build and enhance the sustainable product lines that are important to shareholders, management, and customers.”

Stuart Sanford, Vice President at Mazzone & Associates added “This is a great outcome for all parties. It is even more impressive if you consider that the deal was completed with an international buyer during the COVID-19 pandemic, which disrupted sustainability regulations, supply chains, and customers’ forecasts.”

Founded in 1989, Roplast is a leader in providing sustainable flexible packaging in the form of polyethylene film, bags and other flexible packaging. Based in Oroville, CA, the Company is a leader in providing certified recycled content in its packaging for its customers as well as developing closed loop solutions for the circular economy. Roplast manufactures, converts, and prints its products for a variety of markets.

Industry Insights: Global Packaging Update Winter 2021

With 2020 finally behind us, we can see how the global pandemic impacted the packaging industry and, more specifically, packaging mergers & acquisitions. Overall, Packaging fared better than many sectors of the economy. This was in part driven by a large portion of packaging destined for inelastic markets such as food, personal care, and healthcare as well as a favorable raw material environment for the better part of the year. However, a deeper dive into the various packaging end markets leads to a wide array of year-over-year results for sales and volumes.

With 2020 finally behind us, we can see how the global pandemic impacted the packaging industry and, more specifically, packaging mergers & acquisitions. Overall, Packaging fared better than many sectors of the economy. This was in part driven by a large portion of packaging destined for inelastic markets such as food, personal care, and healthcare as well as a favorable raw material environment for the better part of the year. However, a deeper dive into the various packaging end markets leads to a wide array of year-over-year results for sales and volumes.

Industry Insights: Global Packaging Update Summer 2020

As we now enter the seventh month of our pandemic-induced recession, we find ourselves still dominated by uncertainty – uncertainty in our COVID-19 recovery timeline, uncertainty in our economic recovery, and uncertainty about the long-term impacts of changes in how society will operate in the future. With several months of data now available, we can now begin to assess how has this impacted M&A for the Packaging Industry.

As we now enter the seventh month of our pandemic-induced recession, we find ourselves still dominated by uncertainty – uncertainty in our COVID-19 recovery timeline, uncertainty in our economic recovery, and uncertainty about the long-term impacts of changes in how society will operate in the future. With several months of data now available, we can now begin to assess how has this impacted M&A for the Packaging Industry.

2020 Q1 Industry Insights: Packaging

As of this writing, we are in the early stages of “lock down” as a result of the COVID-19 outbreak. While we cannot be certain of either the severity or duration of the impact, it is safe to say that no one in our Industry is immune to COVID-19’s effects.

Upcoming Industry Events

AWA Global Release Liner Conference, February 27-28 (Presentation Available upon Request)

AIMCAL Executive Conference Webinar, April 9

Packaging M&A Webinar, May 18

International Sleeve Label Conference, November 2

PACKAGING M&A OVERVIEW

As of this writing, we are in the early stages of “lock down” as a result of the COVID-19 outbreak. While we cannot be certain of either the severity or duration of the impact, it is safe to say that no one in our Industry is immune to COVID-19’s effects. Anecdotally, within the last two weeks:

A client serving the retail market is adjusting its customer mix as the shift from brick-and-mortar to online shopping accelerates in the near term

An overseas client is deferring strategic acquisition plans until the impacts of the virus become clearer

A packager of household cleaners is enjoying record volumes and is now seeking to acquire capacity

A packaging equipment client is reassessing timing of capital needs following the postponement of an industry conference to 2021

Overall, Packaging should be less impacted than many other sectors of the market, as (i) it is largely a “local business” with relatively less cross-border or cross-region shipping and supply chain reliance, and (ii) large portions serve cycle-resistant markets such as food & beverage, healthcare, and personal care. Given this, we suspect that Packaging – and the transaction market behind that – will rebound quickly as the virus subsides. In the interim, we expect deal flow to slow substantially as uncertainty hinders decision making.

Please note that the following data is largely “pre-COVID-19” – the impact of the virus will largely be exhibited in data beginning in March 2020. Nevertheless, it can be used by Buyers and Sellers to understand underlying transaction dynamics for when the market returns.

Before the onset of COVID-19, Mazzone highlighted three key trends impacting Packaging companies’ performance and transaction prospects in 2020:

A benign raw material pricing environment is providing margin tail winds for many converters. Among plastic resins, most all packaging grades fell meaningfully in 2019, with many grades continuing this trend into Q1-2020. Paperboard and Linerboard inputs, while not witnessing the same level of decrease, generally enjoyed flat to slightly down pricing. A softening demand (COVID-19 impact) and decreased energy/freight prices (OPEC/Russia price war) could prolong this environment. Buyers are intensifying their due diligence to ensure that current margins are sustainable in the event of (a) a rebound in raw material costs, and (b) demands from customers to pass along these cost decreases.

The search for more sustainable packaging options has created uncertainty regarding the future of certain packaging formats, most notably single use plastics. This uncertainty was amplified in 2019 as state lawmakers introduced no less than 95 bills related to the regulation of plastic bags alone. The inconsistency of state and municipal regulation (and the ability to effectively enforce them) has added further confusion to the market. Investors are seeking to understand the full extent of the shift, so that they can identify the winners and losers among various packaging formats.

2019 saw continued high leverage among packaging companies. Among public packaging companies, Net Debt / EBITDA continued to inch up, reaching 3.7x versus its three-year average of 2.8x. Among Leveraged Finance Transactions (LBOs), average leverage exceeded 5.0x among all disclosed US transactions (not packaging-specific). This heightened level of leverage is manageable in an environment with both low interest rates and a growing economy. As the latter is now greatly at risk, highly levered companies may find themselves capital constrained and/or exceeding covenants as we enter Q2 and Q3 of 2020.

DEAL VOLUMES & PRICING

As the graph below illustrates, global transaction volumes among industrial companies entered a decline well before COVID-19. In the previous cycle, the prior deal volume peak (2007) fell by 30% in 2009 but rebounded in 2010, generally following changes in GDP. Our most recent industrial deal volume peak, however, was in 2015. Transaction volumes have since fallen in each year despite an overall growing economy (and before any COVID-19 impact). Packaging resisted from this trend. In fact, deal volumes have grown year over year including a 14% increase in deal volume from 2018 to 2019.

2020’s early volumes indicate that this may no longer be holding. Volumes for the first two months of 2020 are down 30% from 2019 – with this is largely pre-dating any impact from COVID-19. While we suspect that this gap may narrow as more data comes in, we believe that COVID-19 will reinforce this negative trend as we enter March and April. Nevertheless, we believe that Packaging deal volumes will suffer less than overall deal volumes given that Packaging is overall a more recession-resistant segment of industrials.

Pricing (as determined by transaction multiples) increased by a half turn of EBITDA over 2018’s levels, with median multiples of 9.1x EBITDA and 1.5x Revenue for 2019. Factors continuing to support high levels of pricing include accommodative leverage, a high level of interest from both financial and strategic buyers, ongoing consolidation in those segments of packaging which remain relatively fragmented, and the underlying attractiveness of an industry that consistently offers resilient margins and GDP+ growth. The sustained healthy pricing in this Seller’s Market may also have contributed to lower transaction volumes in early 2020, as buyers wait for more conducive deal metrics (a Buyer’s market).

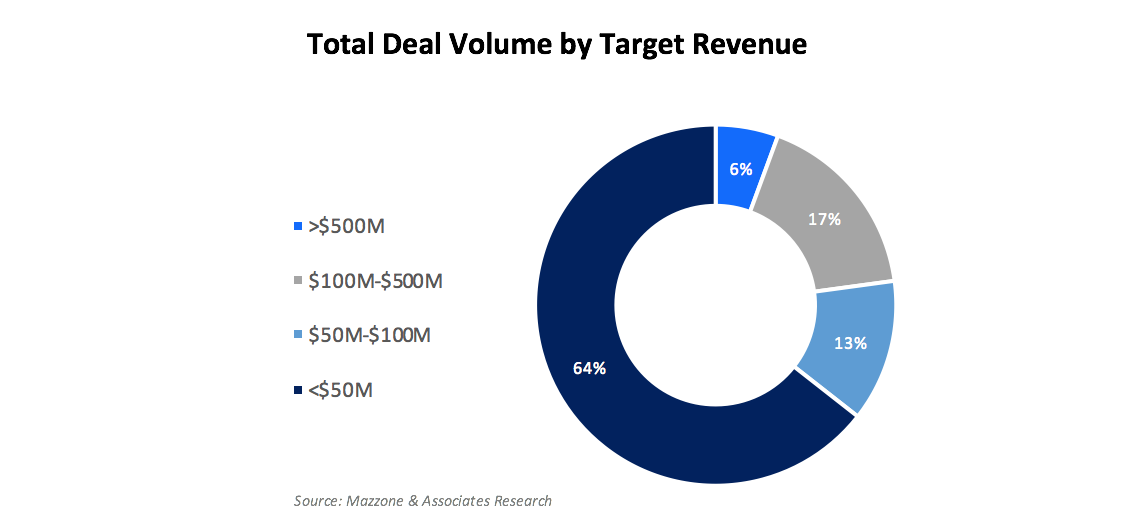

DEAL VOLUME BY TARGET SIZE

There is a healthy market across the spectrum of company sizes, but the greatest activity remains among the smallest companies. Almost two-thirds of disclosed transactions were targets of less than $50 million in revenue, with the majority of these at or below $20 million. While certain sectors such as Glass and Cans have essentially consolidated, there remains tremendous consolidation activity among other sectors, with these smaller tuck-in deals common among paper-based, labels, flexibles, rigid plastics, machinery and distribution companies.

Our analysis indicates that for Pricing, size does matter. Smaller deals (target revenue under $100M) trade at a 1x discount to the overall median of 9.1x. Larger deals, those of targets with revenues above $100 million, trade at a 1x premium (10x+). This differentiation by deal size supports consolidation strategies, as Consolidators seek to arbitrage the multiple expansion to enhance investment returns.

BUYER & SELLER ANALYSIS

Private Equity investors, including both new buyouts and add-ons to existing platforms, accounted for 48% of 2019’s transactions, with Corporate Buyers accounting for 28% and Private Company buyers 24%. These splits are consistent with data from the last five years. We attribute the high participation rate for Private Equity Buyers to:

stable growth and profit margins providing a “defensive investment,”

availability of leverage,

relatively low capex compared to cash generation (particularly in private equity-favored sectors such as Flexibles), and

ability to leverage add-ons and arbitrage size multiples upon exit.

Among Sellers, Private Companies comprised 65% of all transactions, with Corporates and Private Equity splitting the remainder. Private Equity exits are largely to other sponsors, with these secondary transactions accounting for 58% of private equity exits.

As it regards Pricing, 2019 data runs counter to the orthodox view that industry incumbents are better placed to pay higher prices due to their ability to extract synergies from an acquisition. As compared to their corporate and private competitors, financial sponsors pay an additional turn+ of EBITDA, not only for add-ons but also for new platforms. We see this as evidence of their need to deploy capital in a strong seller’s market. The same pricing disparity between Private Equity and other parties exists when the exit their investments, i.e., while Private Equity buyers pay a premium, that same premium exists when they sell (often in secondary buyout to another private equity sponsor).

DEAL MOTIVATIONS

To better understand the drivers for transactions, we identify apparent motivation(s) of the Buyer in Packaging M&A, grouping them into four general categories. The most common motivation is Consolidating Market Share, followed by Product/Market Expansion and Geographic Expansion, and lastly, by Financial (which includes not only Private Equity Platforms, but also IPOs, private investor acquisitions, etc.). Please note that due to multiple potential motivations for a given transaction, the total exceeds the 270 transactions noted for 2019.

The highest valuations include those driven by Financial Motivations (as echoed in our Buyer Analysis for Private Equity acquisitions) and in Product/Market Expansions, which we interpret as the most compelling strategic transactions. Those sectors seeing the most consolidation activity are the Paper, Flexibles, Distribution, and Labels sectors.

SUMMARY

Overall, volume and valuations remained robust in the Packaging M&A space through the end of 2019. Furthermore, several transformative acquisitions have closed/are anticipated to close in 2020:

In Rigid Plastics, Clearlake’s secondary buyout of Pretium Packaging from Genstar Capital

In Flexible Paper, Hood Packaging’s acquisition of TC Transcontinental’s Paper & Woven Polypropylene Packaging operations

In Rigids + Flexibles, Liqui-Box Holdings (Olympus Partners) acquisition of DS Smith’s Plastics Division (as well as the acquisition of certain Rapak operations by TriMas as a regulatory condition of Olympus’ transaction)

In Folding Cartons, Graphic Packaging Holding’s pending acquisition of Greif’s Consumer Packaging Group

In Flexibles, Partner’s Group pending secondary buyout of Schur Flexibles from Lindsay Goldberg

In Rigid Plastics, Silgan’s pending acquisition of Albéa’s Dispensing Business from PAI Partners

In Other Rigids, the pending acquisition of Owens-Illinois Australian and New Zealand operations.

Through 2019 and into early 2020, we continued to see sustained interest in the packaging industry from both strategic and financial investors, as buyers seek to consolidate segments and diversify geographies, markets, and technologies. While the current environment is unsettled, we believe that the underlying trends in in the Packaging space will bring acquirers back to the market as soon as later this year.